Audits for temporary staffing insurance ensure your premiums align with your actual payroll, classifications, and operations. These audits prevent overpayment, highlight compliance issues, and flag risks like uninsured subcontractors or worker misclassification. To prepare effectively:

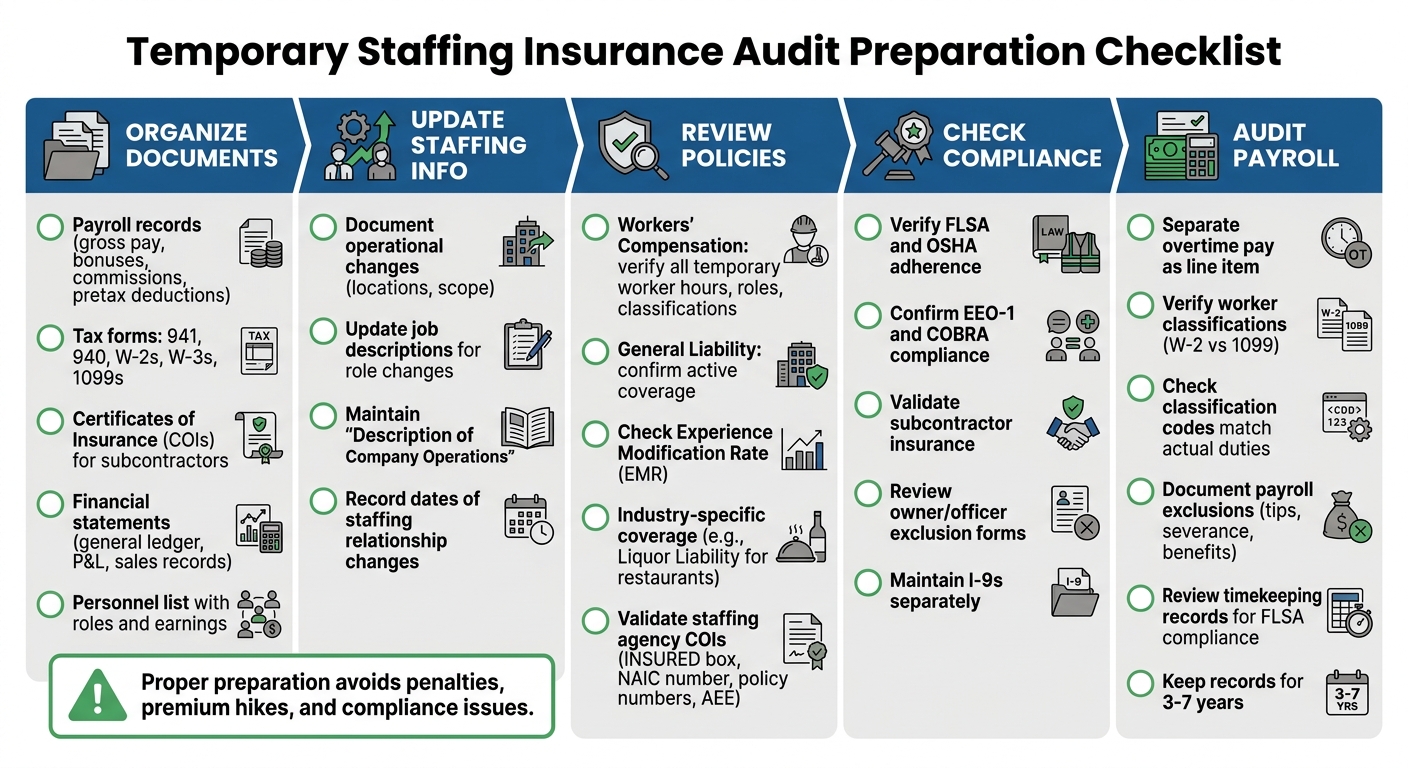

- Organize Documents: Gather payroll records, tax forms (941, 940, W-2s, 1099s), Certificates of Insurance (COIs), and financial statements.

- Update Staffing Info: Document operational changes, job descriptions, and classification codes.

- Review Policies: Ensure Workers’ Compensation and General Liability policies reflect accurate roles and hours.

- Check Compliance: Verify adherence to labor laws (FLSA, OSHA) and confirm subcontractors’ insurance validity.

- Audit Payroll: Separate overtime, check exclusions, and ensure classifications match duties.

Proper preparation avoids penalties, premium hikes, and compliance issues. Digital tools can streamline audits and help manage records efficiently.

Temporary Staffing Insurance Audit Preparation Checklist

Insurance Audits: The Secret That Could Save You Thousands

sbb-itb-d1a6c90

Preparing for Your Audit

Getting ready for an audit can make the process smoother and help you avoid unnecessary mistakes. Auditors will need to verify payroll details, classification codes, and subcontractor insurance coverage. By organizing everything ahead of time, you can save yourself from delays and potential headaches. Here's a practical checklist to help you prepare your documents and records efficiently.

"Providing incorrect information or even glaring errors can prolong the audit process and require you to resubmit documents." - Kelly Spors, ADP SPARK Blog

Collect and Organize Your Documents

Start by pulling together your payroll records. This includes gross pay, bonuses, commissions, and any pretax deductions like Section 125 or 401(k) contributions. Make sure overtime pay is clearly separated as a line item, since many states exclude the overtime premium portion from the audit base. You'll also need to have your tax documents ready, such as Form 941 (federal employer tax returns), Form 940 (unemployment tax returns), W-2s, W-3 summaries, and 1099 forms for contractors.

For subcontractors and staffing agencies, gather Certificates of Insurance (COIs) to confirm they have their own Workers' Compensation and General Liability coverage. Without valid COIs, the auditor may treat these individuals as if they were part of your payroll, which could increase your premium. Additionally, prepare your general ledger, profit and loss statements, service-specific sales records, and a list of key personnel along with their roles and earnings.

Keep all these documents in one well-organized folder. Use simple file names to avoid upload issues. Taking the time to review your tax and payroll records before the audit can help you catch errors early, reducing the chances of resubmitting documents and slowing down the process.

Document Changes in Staffing and Operations

If your business has undergone changes, auditors will need to know. This includes shifts in geographic locations, adjustments in staffing relationships, or changes in the scope of your operations. Maintain an updated "Description of Company Operations" that outlines where your work takes place and the services you provide. For example, if you've added a new location or stopped working with a particular staffing agency, make sure to document the dates and details.

Whenever an employee's role changes, update their job description immediately. These written descriptions are critical for auditors to verify classification codes. Regularly auditing your payroll and tax filings can help you identify and fix any discrepancies before the official audit takes place.

Review Worker Contracts and Classification

Once your documents and operational updates are in order, double-check that all worker contracts accurately reflect their job classifications. Temporary workers, in particular, should be classified based on their actual duties. Since the auditor will calculate your premium by multiplying your payroll by the rate tied to each worker's classification code, mistakes here can be costly. Organize payroll records by employee name, job title, and classification code to make the auditor's task easier.

For subcontractors, ensure their contracts include current COIs and comply with labor laws. If a subcontractor cannot provide proof of insurance, they'll be treated as your employee, and you'll be charged accordingly. Additionally, review your owner and officer exclusion files. If any business owners have opted out of coverage, you'll need signed state-specific exclusion forms and meeting minutes documenting those decisions.

Insurance Policy and Coverage Review

Take time to review your insurance policies to ensure your coverage aligns with your actual operations and meets regulatory requirements. Missing endorsements or incomplete certificates can lead to higher premium costs. Pay special attention to Workers' Compensation to confirm it complies with necessary standards.

Confirm Workers' Compensation Coverage

Your Workers' Compensation policy needs to include all temporary worker hours, job roles, and classifications. Premiums are calculated by multiplying the payroll by a rate tied to each worker's classification code, so getting these details right directly impacts your costs. Double-check that every temporary role is assigned the correct NCCI or state classification code. Misclassifications can result in costly overpayments.

Review your Experience Modification Rate (EMR) as well. This rate reflects your claims history - rates above 1.0 suggest a higher-than-average loss record and will increase premiums, while rates below 1.0 can lower them. Additionally, confirm that your Commercial General Liability (CGL) coverage is active. This policy protects against third-party claims for bodily injury or property damage. If your temporary workers are in the restaurant or bar industry, make sure you also have Liquor Liability coverage to address risks tied to serving alcohol.

Verify EEO-1 and COBRA Compliance

Compliance goes beyond payroll and insurance - it also involves benefits reporting. Temporary workers must be included in compliance reports and benefits regulations. Ensure you're adhering to EEO-1 and COBRA requirements. While these may not directly relate to your insurance policies, auditors might review your records to confirm compliance with federal and state employment laws. Keep detailed records of which workers are covered under each employer’s plan, especially when working with a Professional Employment Organization (PEO).

Validate Staffing Agency Insurance Certificates

Once your records are in order, take a close look at your staffing agency’s insurance certificates (COIs) to avoid misclassification risks or coverage gaps. Ensure the agency’s legal name is listed in the "INSURED" box. As CheckMyCert emphasizes:

"If the name of your Staffing Agency is not in the Insured box, they do not have coverage under the policy number listed on the COI, period".

Key details to verify on each COI include:

- A valid NAIC number that matches the listed insurance carrier. Cross-check this number on your state’s insurance department website to confirm the carrier is authorized to operate in your state.

- Unique policy numbers with validity capped at 12 months. Duplicate policy numbers across different years should raise a red flag.

- A hard copy of the Alternate Employer Endorsement (AEE), which extends the staffing agency’s Workers' Compensation coverage to your business.

"An Alternate Employer Endorsement protects you because an AEE extends workers' compensation coverage to companies that the staffing agency typically does business with".

Don’t just rely on the insurance broker for verification. Contact the insurance carrier directly to confirm that the staffing agency is a listed policyholder and that your company is recognized as a certificate holder.

Payroll and Worker Classification Audit

Once you've prepared your documents and reviewed your insurance policies, the next step is auditing payroll and worker classifications. This process ensures compliance and helps avoid penalties or back taxes. Auditors rely heavily on payroll records to confirm premium calculations and worker classifications, so accuracy is key.

Review Payroll Reports

Start by thoroughly examining your payroll data. This includes all forms of compensation - wages, bonuses, and fringe benefits. Cross-check your payroll summaries against key documents like quarterly federal tax returns (Form 941), year-end wage totals (W-3), and your general ledger to ensure everything aligns.

Pay close attention to how overtime is recorded. In most cases, overtime premiums can be excluded from premium calculations. However, states like Pennsylvania, Delaware, Utah, and Nevada require the full overtime amount to be included. As BlueWave HR explains:

"If your payroll records don't clearly separate regular hours from overtime hours, the auditor will include all of it at the full rate. No separation = no exclusion = you overpay".

Make sure to document exclusions from auditable payroll, such as voluntary tips, severance pay, and employer-paid benefits or retirement contributions.

Once your payroll data is in order, shift your attention to worker classifications.

Confirm Worker Classification Accuracy

Getting worker classifications right is essential to comply with federal and state employment laws. The IRS and Department of Labor use multi-factor tests to determine if a worker is an employee or an independent contractor, focusing on the level of control and independence. Many states add an extra layer of scrutiny with the stricter "ABC test".

Regularly review W-2 and 1099 roles to ensure they meet these legal standards. Check that job descriptions, offer letters, and employment agreements clearly reflect each worker's actual duties and level of independence. Misclassifying workers can lead to hefty consequences, including back taxes and unpaid benefits.

Keep a subcontractor log to track all 1099 workers and ensure each one has a valid Certificate of Insurance (COI). Without a COI, their pay could be added to your auditable payroll at your class code rate. Also, store Form I-9s separately from other personnel files to simplify audit responses.

After reviewing classifications, take a closer look at overtime and shift schedules.

Check Overtime and Shift Schedules

Timekeeping records are essential for verifying compliance with the Fair Labor Standards Act (FLSA) and state labor laws. For hourly workers, use digital time-tracking systems to ensure hours and overtime are recorded accurately.

Confirm that overtime pay adheres to FLSA rules and that your records differentiate between regular hours and overtime. If both your company and a staffing agency control a worker’s hours, wages, or scheduling, you could both be considered joint employers and held liable for overtime violations. Also, check that meal break deductions comply with state-specific laws, as these can vary widely.

For industries like restaurants or hospitality, ensure that voluntary tips are excluded from payroll calculations. However, automatic service charges or gratuities are typically included. Finally, maintain payroll and timekeeping records for 3 to 7 years to be fully prepared for audits.

After the Audit: Reporting and Follow-Up

Finishing the audit is just the first step. Taking swift action afterward is key to preventing future compliance problems. Proper documentation and timely corrections can shield your business from penalties and unexpected premium hikes.

Document Audit Findings

Start by requesting the auditor's worksheet - this will show exactly how your premiums were calculated, including employee classifications, payroll totals, and rate details. Compare this information with your payroll registers, Form 941, state unemployment reports, W-2s, and 1099s. Any discrepancies should be documented right away.

Set up a dedicated exclusion and exemption file. This should include signed state-required exclusion forms, rejection notices, and corporate records for owners or officers who opted out of coverage. For instance, an S-Corp with two officers learned the hard way when it failed to file a required exclusion form for one officer. As a result, the officer's $120,000 salary was added back to the payroll during the audit, leading to an $8,000 premium increase.

Make sure all subcontractor Certificates of Insurance (COIs) are up to date and properly stored. Additionally, keep written job descriptions for each role to support your classification codes in future audits. Maintain payroll and timekeeping records for at least seven years to ensure you're always prepared.

Once your findings are documented, the next step is to address any issues.

Fix Issues and Schedule Follow-Up

If you discover errors in employee classifications or payroll figures, gather supporting documents, such as contracts and job descriptions, and contact your insurance carrier for a formal review. Reclassify workers as needed to avoid penalties, and make sure to act quickly. If you're facing a large audit bill, ask your carrier about flexible payment options.

Correcting worker classifications is especially important to avoid IRS audits or lawsuits. In the staffing industry, misclassification lawsuits have resulted in settlements exceeding $1.2 million to cover back wages and penalties.

Conduct quarterly internal reviews to catch errors in classifications or payroll before your official insurance audit. If your business experiences fluctuating payroll or rapid growth, consider requesting an interim audit from your broker. This can help you determine whether you're ahead or behind on estimated premium payments. Additionally, meet with your insurance broker quarterly to review open claims. Challenge "stale" claims with high reserves that are no longer active. For example, one manufacturer found three claims from five years ago still open with $75,000 in reserves, even though the employees had fully recovered. By providing documentation to close these claims, the company improved its Experience Modification Rate (EMR) calculation.

Once discrepancies are addressed, digital tools can simplify ongoing audit management.

Use Digital Tools for Audit Management

Digital tools can be a game-changer for managing audits and ensuring compliance. Many insurance carriers now offer telephone audits, which allow you to submit all necessary documentation electronically instead of hosting an auditor onsite. Carrier portals also let you manage audit outcomes digitally, including selecting refund options or setting up payment plans.

Keep tabs on payroll during the policy term using this formula: Rate x (Payroll/100) = Premium. As Mordechai Kamenetsky, Co-founder and Lead Agent at Kickstand Insurance, advises:

"Your workers' comp audit bill should never come as a surprise to you. Keep a close watch on your payroll throughout the policy term to make sure that your payroll projections stay accurate".

Platforms like BizBot can help you organize documentation and monitor compliance for future audits. By consolidating your HR, accounting, and management tools, you can maintain accurate records and resolve issues before they escalate. Transitioning to electronic storage and cloud backups for employee records can also improve accessibility and protect against data loss.

Conclusion: Staying Compliant and Reducing Risk

Audits play a key role in ensuring your premiums are accurate. By keeping Certificates of Insurance (COIs) from all subcontractors, maintaining detailed payroll records, and reviewing worker classifications regularly, you can avoid unexpected premium increases and even policy cancellations. Having valid subcontractor COIs is especially important, as it prevents them from being misclassified as employees. A thorough audit process not only ensures accurate premium payments but also shields your business from potential risks.

Regular audits also help safeguard your business from financial and legal issues. Ignoring audit requirements can lead to policy cancellations, fines, or even legal action. Staying ahead with compliance helps you meet regulations while maintaining uninterrupted coverage.

Digital tools can further simplify compliance and reduce future risks. For example, digital audit portals allow you to upload documents electronically, making the process more efficient. Additionally, pay-as-you-go workers' compensation systems calculate premiums based on actual payroll, helping you avoid surprises at the end of the year.

Platforms like BizBot can centralize your HR and accounting documentation, keeping everything organized and minimizing costly errors. By staying on top of documentation and ensuring compliance throughout the year, you'll be ready for audits and better equipped to handle every step of the process.

FAQs

What triggers a temporary staffing insurance audit?

A temporary staffing insurance audit happens when your insurance provider examines details like payroll, employee classifications, and operational data. The goal? To ensure the premium you’ve paid matches your actual risk exposure - things like the number of employees and the type of work they’re doing. These audits play a key role in maintaining accurate coverage and preventing any mismatches in costs or protection.

How do I prove subcontractors aren’t my employees?

To confirm that subcontractors are not your employees, it's essential to have documentation that demonstrates their independent operation. Key pieces of evidence include:

- Contracts or agreements that clearly outline their role as independent contractors.

- Certificates of insurance (COIs) showing they carry their own insurance coverage.

- Proof of independence, such as using their own tools or equipment and managing their own work schedule.

These documents are crucial during audits and can safeguard your business from potential misclassification issues.

What can I do if the audit increases my premium?

If your premium goes up following an audit, take the time to thoroughly review the audit findings. Check for any mistakes by comparing the audit's conclusions with your own records and ensuring they align with your actual business activities. Stay calm and professional throughout the process - avoid speculating or providing irrelevant details. Make sure all the information is accurate before agreeing to the premium increase. If you still find inconsistencies, you can request a review or formally appeal the results through the proper channels.