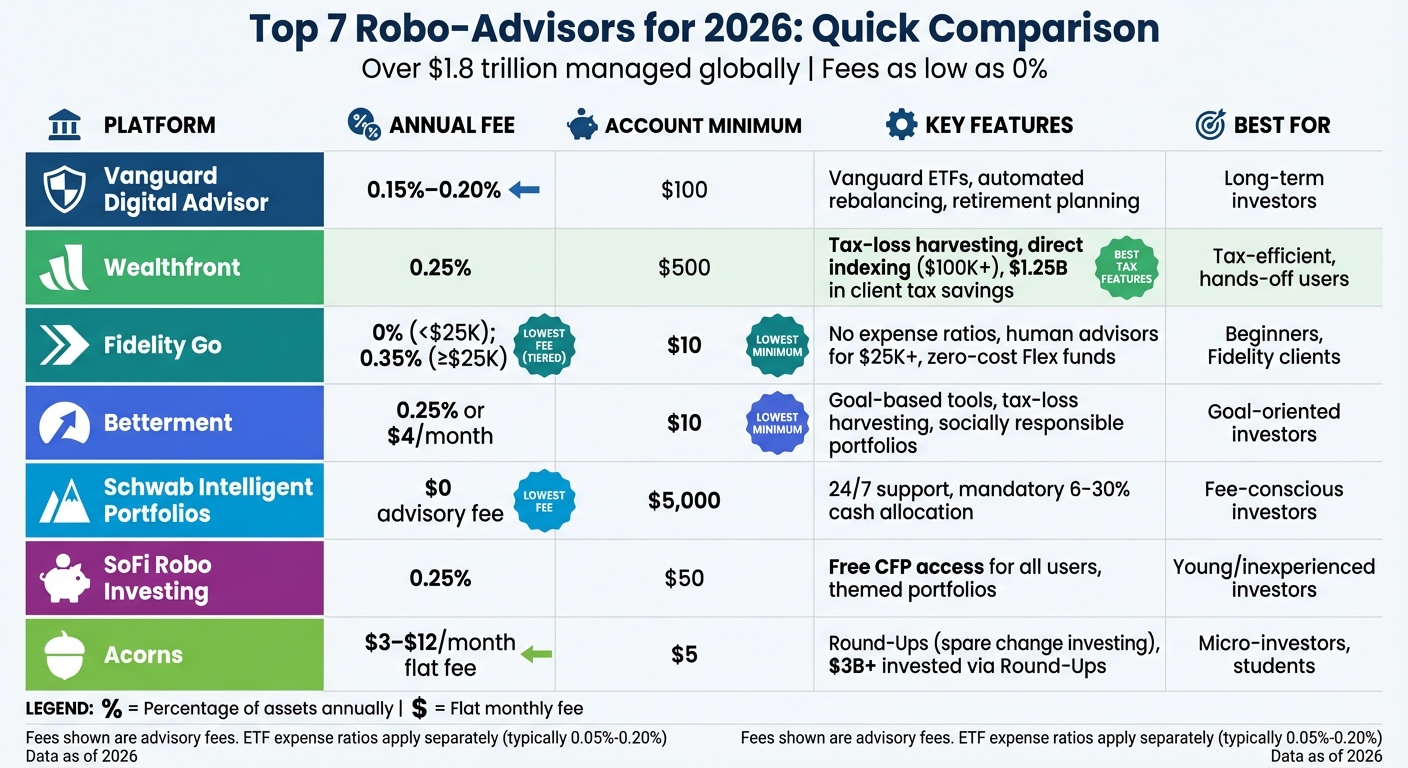

Robo-advisors are reshaping how people invest by offering low-cost, automated portfolio management. In 2026, these platforms manage over $1.8 trillion globally, with fees as low as 0%–0.35% and minimum investments starting at $0. Here's a quick breakdown of the top options:

- Vanguard Digital Advisor: Low fees (0.15%–0.20%), $100 minimum, ideal for long-term investors.

- Wealthfront: 0.25% fee, $500 minimum, strong tax-loss harvesting and direct indexing for accounts over $100,000.

- Fidelity Go: No fees under $25,000, $10 to start, access to human advisors for balances above $25,000.

- Betterment: Flexible pricing (0.25% or $4/month), $10 minimum, goal-focused tools, and socially conscious portfolios.

- Schwab Intelligent Portfolios: No advisory fee, $5,000 minimum, but includes a mandatory cash allocation.

- SoFi Robo Investing: 0.25% fee, $50 minimum, free CFP access for all users.

- Acorns: Flat monthly fee ($3–$12), $5 to start, best for micro-investors with automated "Round-Ups."

Quick Comparison

| Platform | Annual Fee | Account Minimum | Key Features | Best For |

|---|---|---|---|---|

| Vanguard Digital Advisor | 0.15%–0.20% | $100 | Vanguard ETFs, rebalancing, retirement planning | Long-term investors |

| Wealthfront | 0.25% | $500 | Tax-loss harvesting, direct indexing ($100K+) | Tax-efficient, hands-off users |

| Fidelity Go | 0% (<$25K); 0.35% | $10 | No expense ratios, human advisors for $25K+ | Beginners, Fidelity clients |

| Betterment | 0.25% or $4/month | $10 | Tax-loss harvesting, socially responsible funds | Goal-oriented investors |

| Schwab Intelligent Portfolios | $0 | $5,000 | No advisory fee, 24/7 support | Fee-conscious investors |

| SoFi Robo Investing | 0.25% | $50 | CFP access, themed portfolios | Young/inexperienced investors |

| Acorns | $3–$12/month | $5 | Spare change investing, easy setup | Micro-investors, students |

Each platform has strengths tailored to specific needs, from low fees to tax efficiency and beginner-friendly tools. Choose based on your goals, balance, and preferences.

Robo-Advisor Platform Comparison: Fees, Minimums, and Key Features 2026

The Best Robo-Advisors for 2026 (Ranked Worst to Best)

sbb-itb-d1a6c90

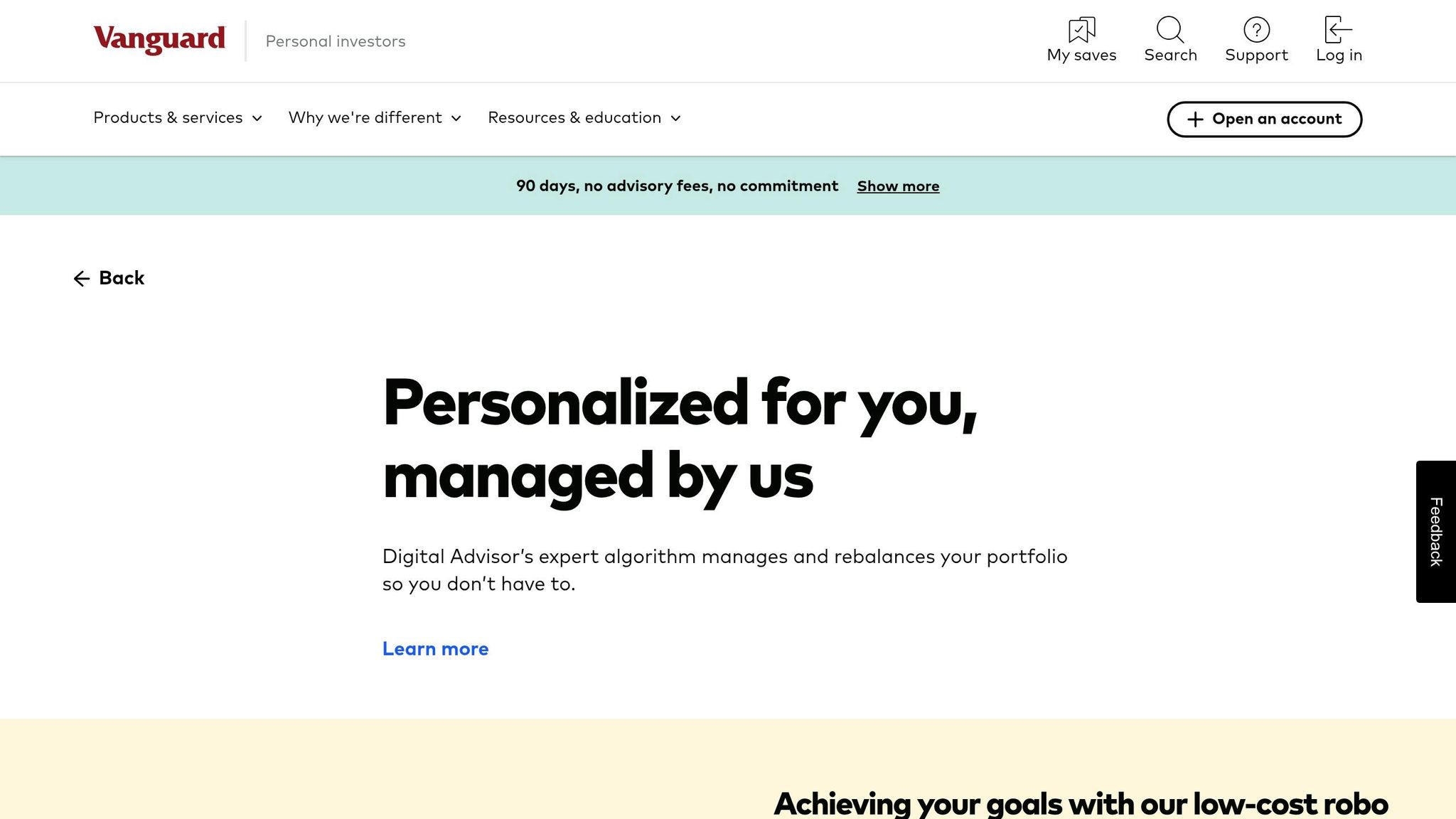

1. Vanguard Digital Advisor

Vanguard Digital Advisor claimed the top spot in Morningstar's Robo-Advisor Landscape Report in January 2025. With an annual fee of just 0.15% to 0.16% for an all-index portfolio, it’s far below the typical 0.25% charged by many competitors. For every $10,000 invested, this translates to about $15–$16 annually.

In September 2024, Vanguard lowered its minimum investment requirement from $3,000 to just $100, making the platform more accessible to a broader range of investors. By June 30, 2024, Vanguard Digital Advisor had over $19 billion in managed assets. Speaking on this change, Brian Concannon, Head of Vanguard Digital Advisor, noted:

"Lowering the investment minimum for Vanguard Digital Advisor is an important step in our endeavor to broaden investors' access to advice, and to empower them earlier in their financial journey".

Here’s a closer look at its fees, features, and suitability.

Annual Fee

Vanguard Digital Advisor offers three portfolio options, each with its own fee structure:

- All-Index and ESG portfolios: Maximum of $20 per $10,000 annually (0.20%).

- Active/Index portfolio: Maximum of $25 per $10,000 annually (0.25%).

New users benefit from a 90-day advisory fee waiver, giving them a chance to explore the platform at no cost. Additionally, Vanguard ETFs come with underlying expense ratios, averaging around 0.05% for all-index portfolios.

Account Minimum

For retail accounts, the minimum investment is just $100, while eligible 401(k) accounts require as little as $5. This low entry point makes it an excellent choice for beginner investors.

Tax-Loss Harvesting

The platform includes automated tax-loss harvesting for taxable accounts. By monitoring your account daily, Vanguard identifies opportunities to offset gains with losses, potentially lowering your tax burden. If your losses exceed gains, you can deduct up to $3,000 of net losses against ordinary income annually, with any excess carried forward to future years. For higher-income investors, the platform also uses tax-exempt investments for U.S. bond allocations in taxable accounts.

Best For

Vanguard Digital Advisor is ideal for long-term, buy-and-hold investors seeking low-cost access to Vanguard's ETF lineup. It’s particularly convenient if you’re already a Vanguard client, as enrolling is seamless for existing account holders. The platform provides over 300 personalized glide paths, adjusting your asset allocation based on factors like age, risk tolerance, and marital status.

However, it’s worth noting that this tier doesn’t include access to human financial advisors. If personalized advice from an advisor is important to you, upgrading to Vanguard Personal Advisor (with a $50,000 minimum) might be a better fit.

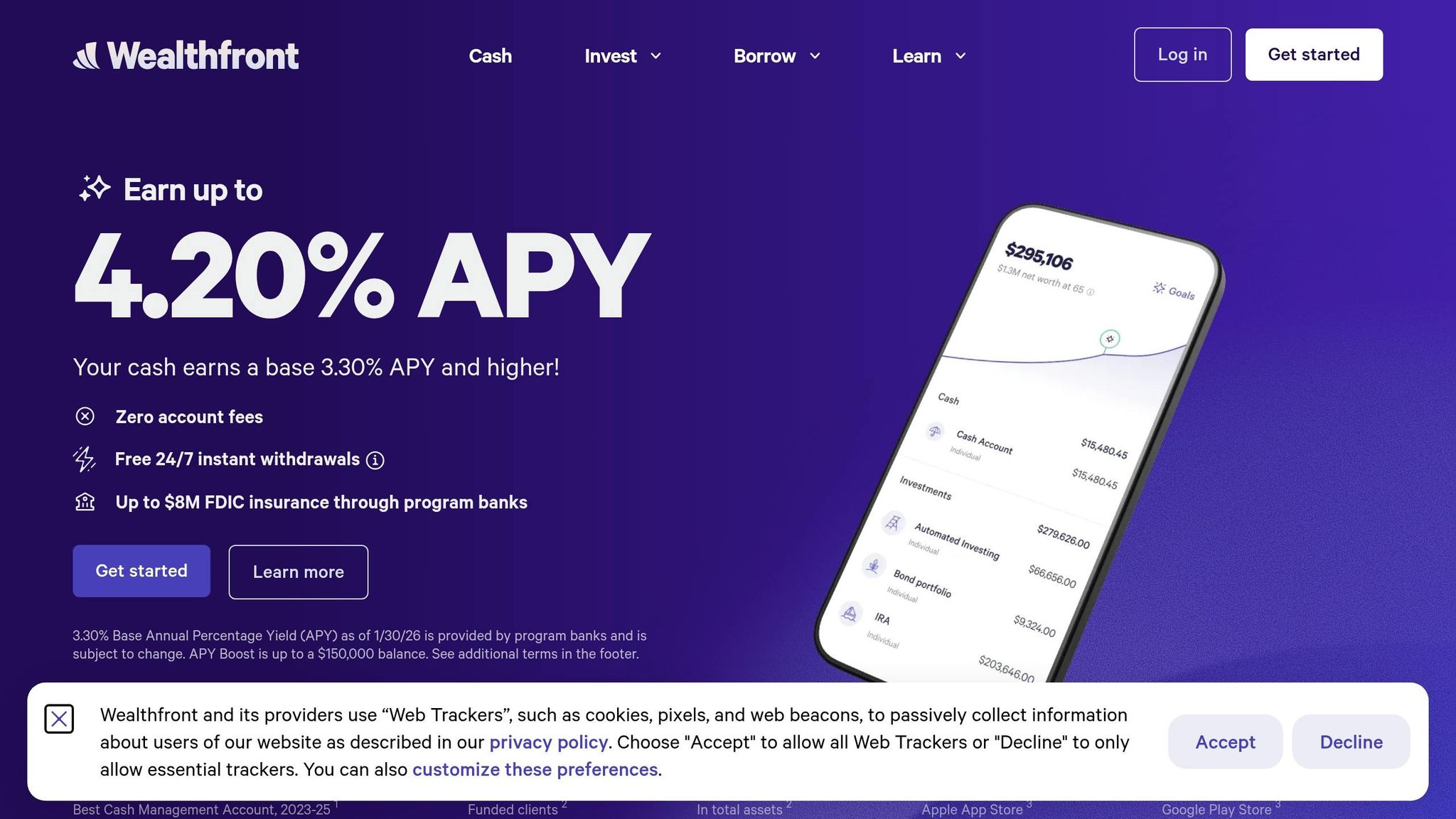

2. Wealthfront

Wealthfront scored a perfect 5.0/5 rating and earned a 2026 Best-of Award for its portfolio options. Known for its cutting-edge tax optimization and automated financial planning tools, the platform has helped clients save an estimated $1.25 billion in taxes since its launch - including $161 million saved in 2025 alone. Let’s break down its fees, account requirements, tax-loss harvesting, and standout features.

Annual Fee

Wealthfront charges a simple flat fee of 0.25% annually, which works out to about $25 for every $10,000 invested. New users can also snag a $50 bonus when they fund their first taxable investment account. Impressively, for around 95% of clients using tax-loss harvesting for at least a year, the tax savings have outweighed the advisory fees.

Account Minimum

Getting started with Wealthfront is accessible, requiring just a $500 minimum investment. The underlying ETF expense ratios typically fall between 0.05% and 0.15%.

Tax-Loss Harvesting

Wealthfront includes daily automated tax-loss harvesting for all taxable accounts at no extra charge. This process involves selling securities that have dropped in value to realize losses, which are then offset by purchasing similar investments to maintain the portfolio’s balance. For example, during three turbulent trading days in 2025, the platform’s system harvested $100 million in losses.

For accounts exceeding $100,000, Wealthfront offers Direct Indexing through options like S&P 500 Direct and Nasdaq-100 Direct. These products allow for tax-loss harvesting on individual stocks rather than just ETFs. Between December 2024 and November 2025, the S&P 500 Direct product alone saved clients an estimated $16 million in taxes. Overall, tax-loss harvesting could add between 0.50% and 1.30% in annual value for investors in tax brackets of 22% or higher.

Best For

Wealthfront caters to hands-off investors who prioritize tax efficiency and appreciate advanced automation over human advisor interaction. Its proprietary Path algorithm connects to external bank accounts, automating transfers based on spending habits to keep as much money in the market as possible. The platform supports a wide range of account types, including taxable accounts, retirement accounts (IRA, Roth IRA, SEP IRA), and 529 college savings plans. However, it’s worth noting that Wealthfront does not provide access to human financial advisors.

3. Fidelity Go

Fidelity Go stands out as a beginner-friendly, cost-effective robo-advisor with a unique tiered pricing structure. It simplifies investing by offering transparent fees and automated features that help optimize tax efficiency. Recognized as Kiplinger’s "Best Robo Advisor of 2025", the platform also boasts a 4.3/5 star rating from Investopedia. Fidelity Go's exclusive zero-expense-ratio Fidelity Flex mutual funds make it particularly appealing to newcomers and loyal Fidelity users.

Annual Fee

Fidelity Go’s pricing is straightforward. For accounts with balances under $25,000, there’s no advisory fee at all. Once your balance hits $25,000 or more, a 0.35% annual fee kicks in - equivalent to $35 for every $10,000 invested. Additionally, Fidelity Go eliminates trading, transaction, and rebalancing fees by utilizing its zero-expense-ratio Fidelity Flex mutual funds.

Account Minimum

Getting started with Fidelity Go is incredibly simple. You can open an account with $0, and it only takes $10 to begin investing. This makes it one of the most accessible options for beginners. If you’re already a Fidelity customer, you can convert eligible brokerage or retirement accounts into Fidelity Go accounts without changing your account numbers.

Tax-Loss Harvesting

For taxable accounts with balances of $25,000 or more, Fidelity Go offers tax-loss harvesting. This feature helps reduce your tax liability by strategically selling investments at a loss to offset taxable gains. However, accounts with balances below $25,000 don’t have access to this benefit.

Best For

Fidelity Go is an excellent choice for beginners, hands-off investors, and existing Fidelity customers looking for a simple, automated way to invest for the long term. With 14 risk levels available for portfolio customization, the platform supports a variety of account types, including taxable accounts, Traditional IRAs, Roth IRAs, Rollover IRAs, SEP IRAs, and HSAs. Once your balance reaches $25,000, you also gain access to unlimited one-on-one coaching sessions with financial advisors at no extra cost. Keep in mind, though, that investment options are limited to Fidelity’s proprietary funds.

4. Betterment

Betterment manages over $65 billion for more than 1 million clients as of late 2025. NerdWallet awarded the platform a perfect 5.0/5 rating in October 2025, highlighting its intuitive design, goal-focused planning tools, and fractional share investing. On top of these standard robo-advisor features, Betterment stands out with flexible pricing options and tailored tax strategies.

Annual Fee

The Digital plan offers two pricing structures: a $5 monthly fee or a 0.25% annual fee, depending on your household balance and deposit habits. If your household maintains a balance of $24,000 or more, or sets up recurring monthly deposits of at least $250, you'll qualify for the 0.25% annual fee. Otherwise, the $5 monthly fee applies, which can result in a higher effective percentage for smaller accounts.

The Premium plan is designed for larger portfolios, requiring a minimum balance of $100,000 and charging a 0.65% annual fee. This tier includes unlimited access to Certified Financial Planners (CFPs) and offers reduced fees for higher balances: accounts between $1 million and $2 million are charged 0.15%, and amounts exceeding $2 million drop to 0.10%.

Account Minimum

You can open an account with no minimum balance and start investing with just $10.

Tax-Loss Harvesting

Betterment enhances investment efficiency with its tax management features. The platform continuously harvests losses in taxable accounts, helping offset capital gains or up to $3,000 of ordinary income. It also offers a "Tax-Coordinated Portfolio" strategy and a "Tax Impact Preview" tool, which shows potential tax consequences before you make transactions.

Best For

Betterment is ideal for beginners, retirement planners, and socially conscious investors. Its automated rebalancing and "set it and forget it" approach make it appealing to those who prefer a hands-off strategy. Goal-oriented savers can take advantage of planning tools to track progress toward retirement, emergency savings, or major purchases. For investors focused on values-based strategies, Betterment provides three socially responsible portfolio options: Broad Impact, Climate Impact, and Social Impact. Premium clients also benefit from unlimited phone and video access to CFPs, making it a strong choice for high-net-worth individuals with complex financial needs.

"Betterment provides options for investors of all net worths and financial priorities. The core service's low expense ratios and account management fees are particularly notable, allowing investors to keep growing their money instead of diverting it to service fees." - June Sham, Lead Investing Writer, NerdWallet

5. Schwab Intelligent Portfolios

Schwab Intelligent Portfolios stands out with its $0 advisory fee, making it an attractive choice for budget-conscious investors. While you’ll still cover the operating expenses of the underlying ETFs - averaging around 0.12% annually - the lack of a management fee is a compelling feature. However, opening an account requires a minimum investment of $5,000, which is higher than some competing platforms. Below, we’ll break down its fees, account requirements, tax features, and who might find it most appealing.

Annual Fee

Schwab doesn’t charge an advisory fee, but it does rely on a mandatory cash allocation to generate revenue. Between 6%-30% of your portfolio is placed in an FDIC-insured cash account. While this allocation is secure, it typically earns less than fully invested alternatives - a phenomenon often referred to as "cash drag." Aside from this, the only fees you’ll encounter are the expense ratios of the ETFs, many of which are Schwab’s own low-cost options.

Account Minimum

To get started, you’ll need at least $5,000. While this minimum might deter some, it remains manageable for many investors. Schwab has earned recognition for its beginner-friendly approach, including a 4.9/5 rating from The Motley Fool in February 2026, which named it "Best for Beginners". The platform also offers 24/7 U.S.-based customer support via phone and live chat, adding a layer of convenience for users.

Tax-Loss Harvesting

Schwab Intelligent Portfolios offers tax-loss harvesting, but it’s only available for accounts with a minimum balance of $50,000, and you’ll need to manually activate the feature. For instance, a $100,000 account recently harvested nearly $18,000 in losses over a few months, showing how this tool can reduce taxable gains.

"The number of tax-loss harvesting trades across Schwab Intelligent Portfolios accounts that are enrolled in the service have historically surged when markets turn turbulent."

- Charles Schwab Investment Management

Best For

This platform is ideal for cost-sensitive investors who can meet the $5,000 account minimum and value 24/7 human support. For those with accounts exceeding $50,000, tax-loss harvesting becomes a useful feature - though it requires manual activation. Schwab Intelligent Portfolios is particularly appealing to beginners who want automated investing without ongoing management fees. However, the mandatory cash allocation means your portfolio won’t be fully invested, which is worth considering.

6. SoFi Robo Investing

SoFi Robo Investing is a solid choice for beginners, thanks to its low $50 account minimum. It earned a 4.5/5 rating from Investopedia in March 2026 and was named "#1 Robo-Advisor of 2025" by Barron's. One standout feature is its access to Certified Financial Planners (CFPs). Every member gets one free 30-minute session, while SoFi Plus members (those with direct deposit) enjoy unlimited consultations. Below, we’ll break down its fees, account requirements, and key features.

Annual Fee

Since November 2024, SoFi has applied a 0.25% management fee. Additionally, investors pay underlying ETF expense ratios, which vary depending on the portfolio theme:

- Classic: 0.07%–0.20%

- Classic with Alternatives: 0.18%–0.46%

- Sustainable: 0.12%–0.17%

Account Minimum

With just $50 to open an account, SoFi is more accessible than many competitors with higher thresholds. It also offers a 1% match on IRA contributions and rollovers. However, keep in mind that an outgoing transfer fee of $100 applies.

Tax-Loss Harvesting

One notable drawback is the lack of tax-loss harvesting, a feature offered by competitors like Wealthfront and Betterment. June Sham, NerdWallet’s Lead Investing Writer, highlights this limitation:

"There are a few drawbacks - the $1 account minimum has been replaced with a $50 minimum, and there is now a 0.25% management fee. There also isn't an option for tax-loss harvesting... more experienced investors might find SoFi less attractive because of this limitation".

While this feature is missing, SoFi focuses on its strength in tax-advantaged retirement accounts.

Best For

SoFi Robo Investing caters to younger and beginner investors who want an easy-to-use platform with the added benefit of CFP access. Its low entry point and "Classic with Alternatives" portfolio - which includes assets like real estate, private markets, and crypto - make it stand out. However, if tax optimization through tax-loss harvesting is essential, other platforms might be better suited for managing large taxable accounts.

7. Acorns

Acorns operates on a flat monthly subscription model, offering three tiers: Personal at $3, Family at $6, and Gold at $12 per month. This translates to an annual cost of $36–$144. However, for smaller portfolios, the percentage cost can be high. For example, a $1,000 portfolio incurs an annual fee of 3.6% under the $3 plan, which is significantly higher than the approximate 0.25% charged by many other platforms.

Annual Fee

The flat-fee subscription includes portfolio management and rebalancing. The Gold tier, priced at $12 per month, comes with extra perks like $10,000 in life insurance, free will planning, and a debit card for kids. Keep in mind that ETF expense ratios still apply, and transferring ETFs costs $35 per fund. This pricing structure, paired with low entry requirements, makes Acorns accessible for those just starting out.

Account Minimum

Acorns has no minimum balance requirement to open an account, but you’ll need at least $5 to begin investing. One of its standout features is Round-Ups, which automatically invests spare change by rounding up your everyday purchases to the nearest dollar. Impressively, as of 2026, this feature has facilitated over $3 billion in investments. For those looking to speed up their savings, the Round-Ups Multiplier lets you double, triple, or even multiply your contributions by 10x.

Tax-Loss Harvesting

Unlike platforms such as Wealthfront, Betterment, and Schwab Intelligent Portfolios, Acorns does not provide tax-loss harvesting. This omission may be a drawback for investors who prioritize tax efficiency.

Best For

Acorns is an excellent choice for beginners, students, and micro-investors who find it challenging to save consistently. Its automated Round-Ups feature makes investing effortless, earning the platform high praise, including 4.5/5 ratings from both Investopedia and InvestLane in 2026. While Acorns simplifies the investment process and stands out for its flat-fee model, it may not be the best fit for investors with larger portfolios or those seeking advanced tax optimization features, such as tax-loss harvesting. Its strengths lie in its ease of use and focus on small-scale, automated investing.

Platform Comparison

Selecting the right robo-advisor comes down to your account balance, budget, and investment objectives. The table below provides a side-by-side comparison of seven platforms, helping you pinpoint the one that aligns with your needs.

| Platform | Annual Fee | Account Minimum | Key Features | Target User |

|---|---|---|---|---|

| Vanguard Digital Advisor | ~0.15%–0.20% | $100 | Uses Vanguard ETFs; automated rebalancing; retirement planning tools | Long-term, buy-and-hold investors |

| Wealthfront | 0.25% | $500 | Tax-loss harvesting; direct indexing ($100,000+); 529 plans; portfolio line of credit | Hands-off investors seeking tax efficiency |

| Fidelity Go | 0% (<$25,000); 0.35% (≥$25,000) | $0 ($10 to invest) | No expense ratios (Flex funds); access to human advisors for balances above $25,000 | Beginners and existing Fidelity customers |

| Betterment | 0.25% or $4/month | $0 ($10 to invest) | Goal-based tools; tax-loss harvesting; crypto and socially responsible portfolios | Goal-oriented investors at any level |

| Schwab Intelligent Portfolios | $0 | $5,000 | 24/7 live support; automated rebalancing; mandatory cash allocation (6%–30%) | Fee-averse investors with higher balances |

| SoFi Robo Investing | 0.25% | $50 | Complimentary access to human financial planners; high-yield savings integration; themed portfolios | Young investors and SoFi members |

| Acorns | $3–$12/month | $0 ($5 to invest) | Round-ups (spare change investing); educational content; IRA match (select tiers) | Micro-investors and beginners |

The table gives a quick overview, but let’s dive into some details to better align these platforms with your strategy.

Fidelity Go is a standout for beginners, offering no management fees for balances under $25,000 and requiring only $10 to start investing. On the other hand, Schwab Intelligent Portfolios is fee-free but has a $5,000 minimum and requires a 6%–30% cash allocation, which some argue could limit long-term growth. For those seeking tax efficiency, Wealthfront and Betterment include automated tax-loss harvesting, which could increase after-tax returns by up to 0.77% annually for higher-income investors. However, not all platforms provide this feature.

Acorns, while beginner-friendly with its round-up investing, can be costly for small balances. For example, its $3 monthly fee equates to 3.6% annually on a $1,000 portfolio. In contrast, Betterment offers more flexibility, charging either 0.25% annually or a flat $4 monthly fee. Meanwhile, SoFi sets itself apart by giving all members complimentary access to Certified Financial Planners, a service that typically requires higher balances or premium fees on platforms like Betterment and Schwab.

"The difference between paying 0.40% annually versus 0.10% might seem small, but over 30 years, we're talking about six figures."

– Reuben Cano, Senior Writer, InvestLane

Conclusion

When choosing a robo-advisor, focus on your financial goals, account balance, and investment timeline. For those just starting out, Fidelity Go and Betterment stand out with their $0 minimum balance requirements and $10 entry point. If you're planning for retirement and prefer a hands-off approach, Vanguard Digital Advisor offers low fees (0.15%–0.20%) and decades of expertise in index fund management.

If you're investing in taxable accounts, tax efficiency is crucial - especially for higher earners. Platforms like Wealthfront and Betterment provide automated tax-loss harvesting, while Wealthfront takes it a step further with direct indexing for accounts over $100,000. This allows for loss harvesting at the individual stock level, not just at the ETF level.

For those prioritizing low fees, Schwab Intelligent Portfolios offers $0 advisory fees for balances above $5,000. However, its mandatory 6%–30% cash allocation might limit growth potential over the long term. On the other hand, SoFi Robo Investing provides access to Certified Financial Planners (CFPs) for all account sizes - something typically reserved for accounts with $100,000 or more elsewhere.

Your choice should reflect your specific needs. For example, Acorns is ideal for automatic round-ups from everyday purchases, Wealthfront's "Path" tool is great for retirement planning tailored to complex lifestyles, and Betterment excels in helping users manage multiple financial milestones with its "buckets" feature.

With robo-advisors managing over $1.8 trillion globally as of early 2026 - and projections suggesting this figure will rise to $3.2 trillion by 2033 - automated investing has firmly entered the mainstream. Additionally, 63% of Registered Investment Advisors now use AI tools, more than double the adoption rate in 2023. Begin with the platform that suits your current situation, knowing you can always adjust or upgrade as your financial goals evolve.

FAQs

How do I choose the right robo-advisor for my goals?

When picking the right robo-advisor, it’s important to weigh factors like fees, account minimums, user experience, and the features that match your financial goals. Start by defining your objectives - whether it’s planning for retirement, building savings, or growing wealth. Then, compare platforms based on what matters most to you. Some might offer perks like tax-saving strategies, tailored financial plans, or lower costs.

Don’t forget to check the minimum balance requirements and whether the platform provides access to human advisors if that’s something you value. Reading reviews or side-by-side comparisons can also help you zero in on the option that feels right for you.

Do I need tax-loss harvesting for my account?

Not every robo-advisor in 2026 provides tax-loss harvesting. Whether this feature is necessary for you largely depends on your personal tax circumstances and investment objectives. Before choosing a platform, confirm if it offers tax-loss harvesting and evaluate how it aligns with your overall financial strategy.

How much do robo-advisor fees cost over time?

Robo-advisor fees usually fall between 0.10% and 0.40% annually, but over the course of decades, these seemingly small percentages can grow into a hefty sum. For instance, if your investments are substantial, these fees could amount to six figures over 30 years. When planning long-term investment strategies, it's crucial to factor in these costs to understand their potential impact on your overall returns.